After we tried to understand finance and budget basics in last blog, time to understand the budget process of any organization in general.

The purpose of a

budget process is to provide, in a consolidated form, the necessary guidelines

for annual budget preparation and approval. This guideline will aid in the

preparation of the annual budgeting cycle program that is prepared and

circulated by the CFO.

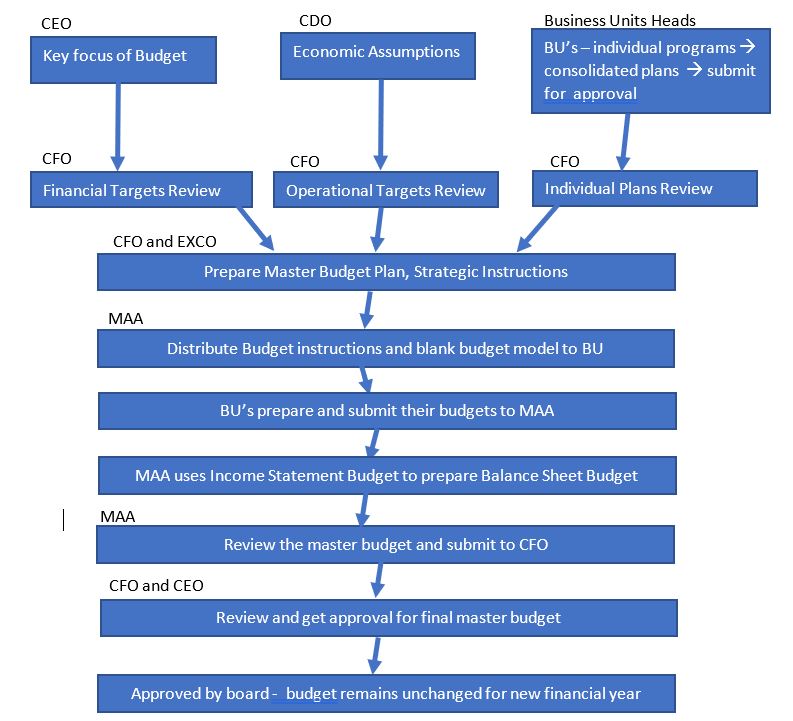

1. Key Stages of the Budget Process

· Meeting of senior management chaired by

CEO to gain a clear understanding of the strategic intent and direction of the Organization

in the next year. Though the budget process is largely driven by the finance

department, it is important for it to have the support of the top management in

the Organization for it to be taken seriously.

· Communication from the CEO to the HOD’s

– Business Units (BU) heads on the strategic intent and key focus of the

budget.

· The Chief Data Officer – CDO will

prepare economic assumptions.

· HOD's and Business Units (BU's) have

the responsibility for developing programs and coordinating the budgets within

their area of responsibility. They will prepare performance analysis of past

immediate period and develop individual annual business plans indicating

clearly the objectives, targets, priorities, actions needed to achieve the

targets, expected results/timelines (if any), and resources needed. A

consolidated proposal will be submitted to Finance.

· CFO will prepare a forecast for current

period to year-end to form basis of comparison for next budget period.

· The CFO will obtain management’s key

financial and operational targets, review the plans and other submissions, and

consolidate the overall Organization master budget.

· Preparation by Finance of the budget

instructions and models to capture the strategic direction from the EXCO

meeting. The key information to be prepared by the CFO are as follows:

· Detailed budget instructions

· Budget preparation matrix

· Budget resource matrix

· Detailed departmental/BU budget model

· Staff cost budget model

· Capex BU and consolidation model

· Guidance notes for budget models

· Consolidation budget model

· Budget reports format for management

· Budget time table

· Detailed budget instructions sent by

the Management Accountant to Budget Holders. The budget instructions will

include a time table and the note will emphasise the importance of meeting the

submission deadline.

· Through a separate note, the Management

Accountant will send the blank detailed budget models together with guidance

notes for the models. Note that models to each department/BU is slightly

modified to suite their requirements.

· BU Budget Holders to gather information

and complete the required sections of the detailed budget model.

· Budget Holders submit their draft

budgets to the Management Accountant for review and inclusion of central costs

(such as insurance) and allocation of shared costs from support Cost Centres.

· The MAA sends back the complete models

to the Budget Holders after inclusion of allocated shared costs so that they

can have a final review of their department’s/BU's overall position.

· Budget Holders submit the final budgets

to the MAA after signed-off budgets by the HOD’s for overall Organization

consolidation.

· The MAA then uses the Income Statement

budget to prepare the budgeted balance sheet in consultation with the business

units.

· During this phase, some Income

Statement numbers such as interest and Organization charges may change due to

budgeting on financing of the business. However, changes to the Income

Statement are expected to be minimal.

· Initially the opening balances used

will be those of the latest balance sheet prepared (usually that of 30th

September) to give a feel of the budgeted balance sheet position. However, the

movement numbers are considered final.

· The budgeted balance sheet is finalised

after the financial year-end when the year-end balance sheet numbers can be

used as opening balances in the budget balance sheet.

· The master budget is reviewed by the

Executive committee (EXCO) for recommendation to the Board.

· Once the Income Statement and balance

sheet budgets are finalised, they are presented to the Board as draft budgets

by the CEO and CFO.

· Review and approval of the overall Organization

budgets by the Board. Once the budgets have been signed-off by the Board, they

cannot be changed for the rest of the new financial year.

· Though the environment is not static,

Budget Holders are expected to put a lot of thought in to their budgets and thus

come up with realistic budgets.

· Any changes to the environment that

significantly alters the key assumptions and parameters used for preparation of

the budgets will be used as explanations to the variances between actual and

budgets. The reason for not allowing changes to the budgets in between the new

financial year is meant to discourage budget holders from requesting for

changes at the slightest excuse when they realise they may not meet their

budget. It is also meant to ensure budget holders take the budget process

seriously knowing their performance will be assessed against the budgets.

· The budgets are important for

operational control and are used as comparatives against actuals in the

management accounts.

2.

Budget Consolidation

· The CFO assisted by the Management

Accountant (MAA) will perform the following:

· Review submissions for consistency with

company’s policy framework, objectives, strategies, goals and targets as well

as contracts and approved maintenance plans, manpower plans, and capital

expenditure plans.

· Check and confirm that the departmental

budgets have been prepared within set parameters and budget guideline earlier

provided.

· Check and confirm appropriateness of

budget allocation costs submitted.

· Seek any points of clarification or

agree appropriate amendments of departmental/BU budgets as applicable with the

Budget Holders.

· Check and confirm consistency and

accuracy of arithmetic computations where applicable.

· Compare consistency with performance

trends.

· Once reasonably satisfied with the

departmental/BU budget submission the CFO consolidates all departmental budgets

into a draft master budget that will be presented to the Executive

committee for recommendation for submission to the Board.

· Although it is the responsibility of

CFO to present the draft consolidated budget, the particular division or

department/BU is still accountable for figures presented and should defend

their budget submission where required.

· The CFO will engage the departmental/BU

heads and agree on revisions so as to align the overall Organization’s Budget.

· Where necessary, the CFO will make

changes to the draft budget as agreed by management. Final acceptance and

approval by management should not be later than one month preceding the

beginning of the financial year being budgeted for.

· The CFO then prepares a budget approval

motivation paper for presentation to the Board Committee and the Board as

applicable. The CFO will present the budget to the Board for approval not later

than one month preceding the beginning of the financial year being budgeted

for.

Once approved by the

Board, the CFO will be responsible for ensuring the budget is uploaded on the

accounting system. The upload will be done per budget line.